Can You Sell Your House With Solar Panels? This Answer Upsets Most Homeowners...

You're ready to sell your house. Maybe you're upgrading, or downsizing, relocating, or just ready for a change.

You call a realtor, start thinking about listing - and then someone asks about the solar panels on your roof.

That's when most homeowners find out what's really in their contract.

What the Home Sale Trap Is, in Plain English

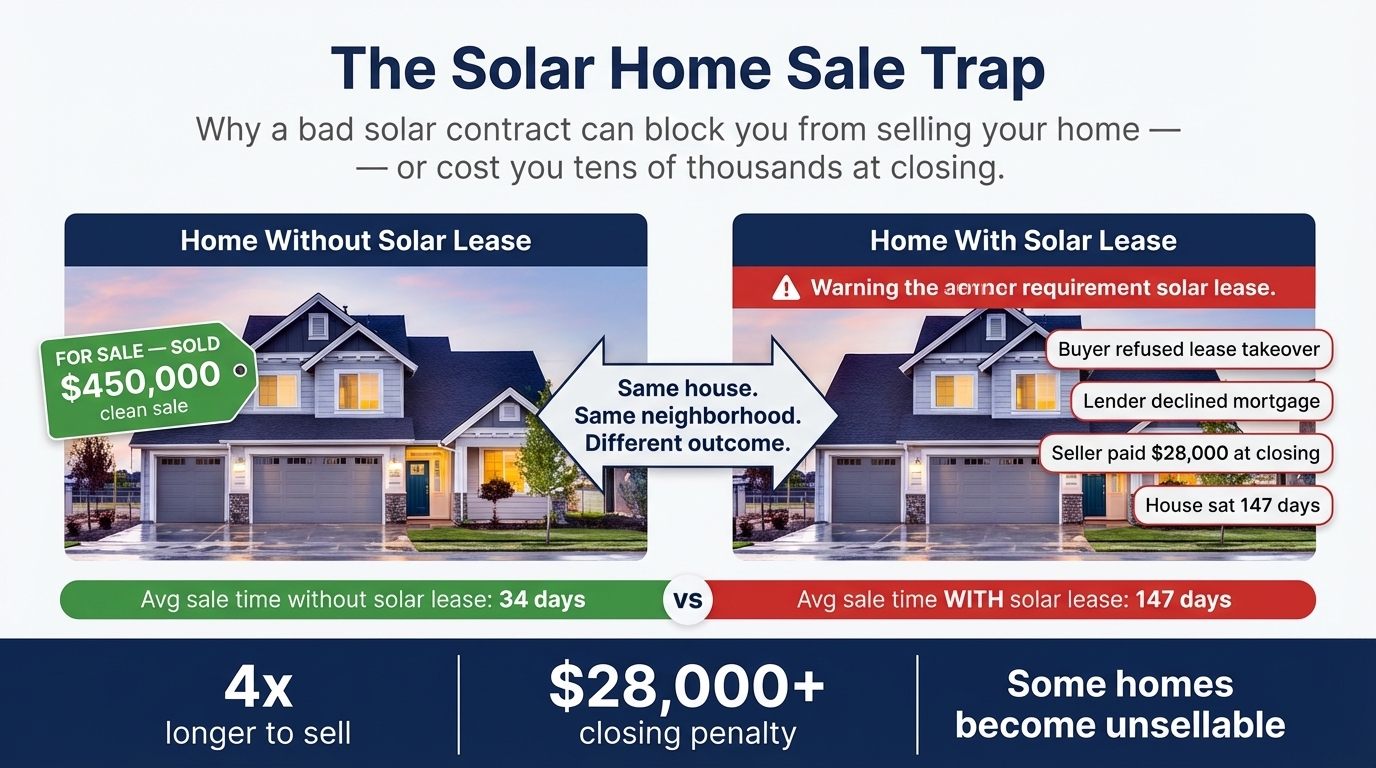

The "home sale trap" is what happens when your solar lease or PPA makes your house harder to sell than the house next door. Your panels are not really yours. The company that owns them has a financial stake in your roof, and that stake rides along with the property. Buyers have to deal with it. Lenders have to deal with it. Title companies have to deal with it. And you and your family are the ones stuck in the middle.

If you own your panels outright (you paid cash or finished paying off a loan), selling is simple. The panels are yours. They stay with the house. They may even add a little value.

But if you signed a lease or PPA, a solar company owns the panels on your roof. That single fact is what creates the trap.

Why This Happens and Who Gets Hurt Most

The residential solar industry grew up fast. Salespeople were trained to close deals, not to walk a homeowner through what happens at resale. The contracts got longer. The escalator clauses got bigger. And nobody at the kitchen table was asked the simple question: what happens when you sell this house in ten years?

Homes with leased solar panels take much longer to sell. Real estate agents around the country report that leased-solar homes can sit on the market three to four times longer than comparable homes without a solar lease. Some deals close at a discount. Others fall apart at the closing table.

This hits one group harder than any other: homeowners 55 and older who are trying to downsize for retirement. AARP has covered the rising pressure on older homeowners to "right-size" their housing as fixed incomes tighten. When a solar lease blocks that move, it's not just a real estate headache. It can delay retirement, drain savings, and force a family to stay in a house they no longer want.

If you and your family are in that spot, you are not alone. You are part of a pattern that the industry created and the industry has been slow to fix.

The Four Main Ways Solar Contracts Block Home Sales

1. The Buyer Refuses to Assume the Lease

When you sell a home with a solar lease or PPA, the buyer has to agree to assume your contract. That means they need to:

- Qualify financially with the solar company (credit check, income verification)

- Accept the remaining term, which could be 15, 20, even 25 years

- Accept the monthly payments, including any escalator clause increases

A lot of buyers walk. Some can't qualify. Some don't want a 20-year obligation attached to a house they just bought. Some already heard a horror story from a friend. Your realtor may have already seen this happen on other listings.

That leaves you waiting, or dropping your price, or both.

2. The UCC-1 Fixture Filing Sits on Your Title Like a Lien

Most solar leasing companies file a UCC-1 fixture filing with the county. This is a notice under the Uniform Commercial Code that says the solar company has a financial interest in equipment attached to your home. It is not the same thing as a mortgage lien, but on a title search it can look a lot like one.

That filing can cause:

- Delays in the title search during closing

- Title insurance companies refusing to insure the transaction until the filing is resolved

- Buyers getting spooked when their attorney flags the filing

- Lenders hesitating to approve the mortgage

Even when everyone agrees the UCC-1 is legal, the paperwork to release, subordinate, or transfer it can add weeks to a closing. Weeks you may not have if you have already bought your next home.

3. Lenders Refuse to Fund the Mortgage

Some mortgage lenders will not fund a loan on a home with an attached solar lease. Fannie Mae has published guidance on how solar leases and PPAs should be treated in mortgage underwriting. The guidance is clear that the lease payment must be counted against the buyer's debt-to-income ratio, and any UCC filing must not impair the first lien position of the mortgage.

In plain English: the buyer has to qualify for the house AND the solar payment. And the lender has to be comfortable that the solar company's UCC filing will not compete with the mortgage. When either one of those tests fails, the loan falls apart. Your pool of qualified buyers shrinks before you even get an offer.

4. You Pay Off the Contract at Closing

If the buyer will not assume the lease and the lender will not fund around it, the final option is usually the worst one: you pay off the entire remaining contract balance yourself at closing. Depending on system size and how many years are left, that buyout can run $15,000 to $40,000 or more.

For a family trying to move because of a job change, a health issue, or a parent who needs care, coming up with that kind of money at the closing table is not a small inconvenience. It can stop the sale cold.

Real Examples and What the Data Shows

This is not a rare event. It is a documented industry pattern.

- The National Association of Realtors has flagged leased solar panels as one of the top non-traditional complications in residential sales, behind only title defects and appraisal gaps.

- The New York Attorney General has brought consumer protection actions against solar companies for failing to disclose how a lease affects resale.

- The California Public Utilities Commission has logged thousands of homeowner complaints tied to leased solar, including failed sales and forced buyouts.

- The Federal Trade Commission has issued residential solar guidance calling out disclosure failures around transfer and buyout terms.

- AARP has published repeated warnings to older homeowners about long-term solar contracts that can complicate downsizing plans.

Real estate agents talk about this quietly. Some will steer buyers away from homes with leased solar rather than try to walk a client through an assumption process that might fall apart at the last minute. That is not fair to you as a seller. But it is the reality your listing is sitting in.

How to Spot the Problem in Your Contract Before You List

Pull out your solar contract before you call a realtor. Look for these sections and this language:

- Transfer or Assignment: rules for transferring the contract to a new owner

- Assumption Requirements: the credit score or income the buyer must have

- Buyout or Early Termination: the formula for paying off the remaining balance

- Fixture Filing or UCC-1: the company's right to file a notice against your property

- Removal: what it costs if you need the panels physically removed

If any of that language is missing, vague, or buried in a schedule at the back of the contract, treat that as a warning sign. The clearest contracts spell out transfer terms in plain numbers. The ones that cause problems tend to leave the math to the solar company.

What You Can Actually Do About It

You have more options than most homeowners realize. What works depends on your state, your contract, and how the panels were sold to you in the first place.

- Request a current buyout figure in writing. Solar companies must provide this on request. The number is often negotiable, especially late in the contract.

- Ask for a partial buyout. Some companies will accept a lump sum to reduce the remaining balance, making the lease easier for a buyer to assume.

- Request a UCC-1 release or subordination. If the filing is blocking a title insurer or lender, the solar company can file paperwork to clear the path.

- Challenge the contract itself. If the sales process involved misrepresentation of resale impact, escalator math, or UCC filings, that may be grounds for a dispute under your state's deceptive trade practices act.

- File a complaint with your state attorney general. Consumer protection divisions in New York, California, Texas, Florida, and Illinois have all taken action against solar companies for sales practice issues.

- Work with a specialist. A senior solar contract consultant can run the buyout math, review your transfer terms, and tell you which path is worth your time.

What To Do Next

- Find your solar contract. If you don't have a copy, request one from your solar company in writing today.

- Look for the transfer, assumption, buyout, and UCC-1 language listed above. Highlight each section.

- Call your county recorder's office or pull your property records online. Check whether a UCC-1 fixture filing is on your title.

- Ask your realtor (or a realtor you trust) how leased solar homes are moving in your market right now.

- Before you list, get a Free Assessment. A senior consultant can review your contract and walk you through what you and your family are actually looking at.

Common Questions About Selling With Solar

Can I sell my house if the panels are leased?

Yes, but the process is more complicated than a standard sale. The buyer usually has to qualify to assume the lease, or you have to buy out the contract at closing, or both.

How much longer does it take to sell with a solar lease?

Industry reports suggest leased-solar homes can take three to four times as long to sell compared to similar homes without a solar lease. Your local market will vary.

What is a UCC-1 fixture filing?

It is a notice that a company has a financial interest in equipment attached to your property. It is filed with the county and shows up on a title search. It acts like a lien in the sense that it has to be cleared, released, or transferred before the sale can close cleanly.

Will my lender let a buyer assume my solar lease?

Some will, some won't. Fannie Mae has underwriting guidance that allows it in certain situations. The buyer's lender makes the final call, and many shy away from leased solar.

How much is a typical solar lease buyout?

Buyouts often run $15,000 to $40,000 or more, depending on system size, years remaining, and the escalator rate. Your contract has a buyout schedule or formula you can request in writing.

I'm 62 and trying to downsize. Do I have any protection?

Your state may have enhanced senior consumer protections. AARP has been active in flagging long-term solar contracts as a risk for older homeowners. A consultant can tell you what options apply in your state.

Can I just remove the panels and sell the house?

Not without the solar company's permission. Removing leased panels usually violates the contract and can trigger penalties, a full buyout, or damage claims. Don't take the ladder out until you have legal footing to do so.

Sources & References

National Association of Realtors, residential transaction guidance. New York Attorney General's office, consumer protection actions. California Public Utilities Commission, complaint database. Federal Trade Commission, residential solar guidance. Fannie Mae, Selling Guide on solar panels and PACE loans. AARP, consumer reporting on long-term contracts affecting older homeowners. State attorney general consumer protection filings in Texas, Florida, and Illinois. Uniform Commercial Code, Article 9 fixture filing provisions.

Thinking About Selling Your Home? Check Your Solar Contract First.

If you have a solar lease or PPA and you're thinking about selling - or if a sale already fell through because of your solar contract - the first step is talking to a senior consultant who can review your situation and tell you what relief you may qualify for.

Free Assessment

Find out what options are available to you. A senior consultant will review your situation and walk you through your next steps.

Most homeowners don't find out their solar contract can block a home sale until they're already trying to sell. By then, the options are expensive.