You Took Out a Solar Loan. Here's What They Likely Didn't Tell You.

If you financed your solar panels with a loan, you were probably told something like this:

"Your solar payment will replace your electric bill. You'll save money from day one."

Sound familiar?

Now here's what's actually happening for thousands of homeowners across the country: you're paying a monthly solar loan payment AND you're still paying a utility bill. The savings your salesperson promised? They never showed up.

And that's only the beginning. There is a good chance your loan also contains a hidden dealer fee you were never told about - a fee that may have added tens of thousands of dollars to what you owe.

What a Hidden Dealer Fee Is, in Plain English

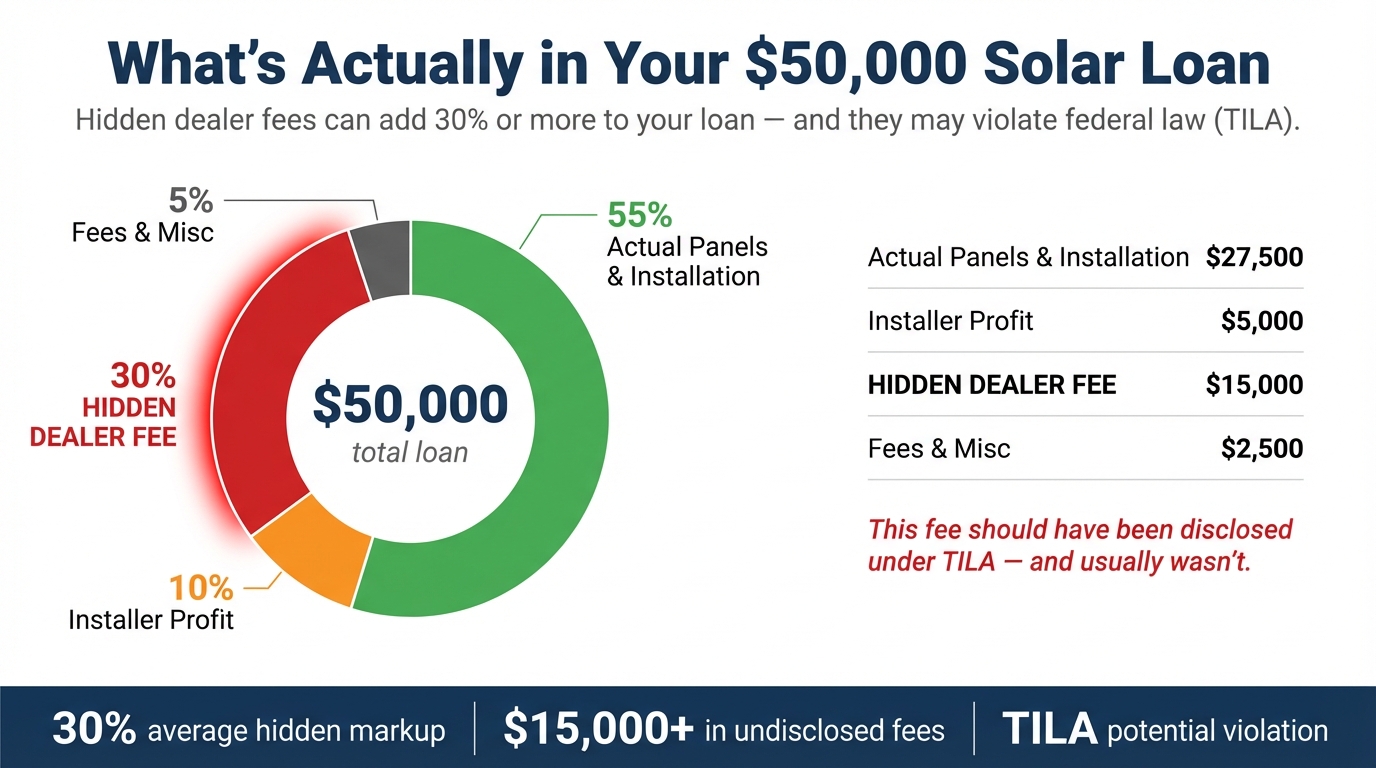

A dealer fee is a markup that the solar lender pays to the installer for bringing in your loan. Think of it as a finder's fee. The lender pays the installer a chunk of money for signing you up, and then rolls that same amount into the total you have to pay back.

Here is the part that catches most homeowners off guard. The dealer fee is usually not shown as a fee on your paperwork. It gets baked into the price of the system itself.

So if a solar company tells you "the system costs $30,000," the real cash price might only be $20,000. The other $10,000 is the dealer fee, silently built into the loan. You then pay interest on that $10,000 for 20 or 25 years.

In the solar financing world, dealer fees commonly run from 20% up to 35% of the loan amount. On some loans they climb higher. That is money added to your balance that does not pay for a single solar panel, inverter, or install crew. It pays the lender for offering you a low advertised interest rate.

Why This Happens and Who It Affects

Almost every solar loan sold at the door or over the phone has a dealer fee built into it. That is how the industry pays for those "1.99%" or "2.99%" teaser rates you see on flyers. The lender is not actually lending you money at 2%. They are lending you money at a normal rate and using the dealer fee to make up the difference.

If you financed your solar system through a company like GoodLeap, Sunlight Financial, Mosaic, Dividend Finance, Sunnova, or a credit union program tied to a solar installer, there is a real chance a dealer fee is sitting in your loan right now.

This affects homeowners of every income level, but it hits seniors and families on fixed incomes the hardest. When you are budgeting carefully, an extra $10,000 or $15,000 quietly added to your loan balance is the difference between saving money on solar and losing money every month for the next two decades.

What the Truth in Lending Act Actually Requires

The Truth in Lending Act, known as TILA, is a federal law. It has been on the books since 1968. Its job is simple. Before you sign a loan, the lender has to tell you the truth about what the loan will cost you.

Under TILA, your lender is required to clearly disclose:

- The amount financed - the actual money being lent to you

- The finance charge - the total dollar cost of credit, including interest and certain fees

- The annual percentage rate (APR) - the true yearly cost of the loan, including fees, not just the interest rate

- The total of payments - what you will pay over the full life of the loan

- The payment schedule - how much and how often

Here is the important part. The APR is supposed to include the dealer fee if the fee is a cost of getting the loan. A 2.99% interest rate with a 30% dealer fee is not a 2.99% loan. Once you properly calculate it, the real APR can be double digits.

If your solar lender showed you a low teaser rate and buried the dealer fee in the system price, and if the APR they disclosed did not accurately reflect what you are really paying, that is a potential TILA violation. And TILA violations carry real consequences for lenders.

Real Examples and Enforcement Actions

Hidden dealer fees in solar loans are not a rumor. Regulators at every level have been documenting and punishing this practice.

- The Consumer Financial Protection Bureau (CFPB) issued guidance in 2023 warning that solar lenders must fully disclose dealer fees and include them properly in APR calculations. The CFPB specifically flagged "hidden markups" in solar financing as a priority enforcement area.

- The New Mexico Attorney General sued a major solar lender for failing to disclose dealer fees that added tens of thousands of dollars to homeowners' loan balances.

- The Connecticut Department of Banking reached a settlement with a solar finance company over dealer fee disclosure failures.

- The Minnesota Attorney General has taken action against solar companies for deceptive financing practices, including hidden fees.

- Class action lawsuits have been filed against GoodLeap, Sunlight Financial, and other solar lenders, alleging TILA violations tied to undisclosed dealer fees.

- The Federal Trade Commission has publicly stated that rolling undisclosed fees into the price of solar systems can violate federal consumer protection law.

The pattern is consistent across states. The homeowner was told one thing. The contract said another. And the dealer fee was doing the heavy lifting in between.

How to Spot a Hidden Dealer Fee in Your Loan Documents

Pull out your loan agreement, your Truth in Lending disclosure, and your installation contract. Look at all three side by side.

First, check the cash price. Somewhere in your paperwork there may be a "cash price" or "system price if paid in cash" figure. If you see one price for cash and a noticeably higher "financed price," the difference is very likely the dealer fee.

Second, do the payment math. Take your monthly payment. Multiply it by the number of months on the loan. Here is an example.

Say your monthly payment is $180 and your loan is 25 years. That is 300 months. $180 times 300 equals $54,000. If your salesperson told you the system cost $30,000, where did the other $24,000 come from? Some of it is interest. A big chunk of it may be the dealer fee plus interest on that dealer fee.

Third, check the APR. If your documents show a very low interest rate but a much higher APR, that gap is usually caused by fees. A 2.99% interest rate with a 9.5% APR is a red flag worth looking into.

Fourth, look for the word "dealer fee," "origination fee," "platform fee," or "program fee" anywhere in the paperwork. Sometimes it is buried. Sometimes it is missing entirely. Both matter.

What You Can Actually Do About It - Including Possible Loan Forgiveness

If your solar loan has a hidden dealer fee that was not properly disclosed, you are not stuck with it. TILA gives homeowners real tools.

Possible remedies may include:

- Rescission. Under TILA, certain loans secured by your home may be rescinded (cancelled) for up to three years after signing if the lender failed to make required disclosures. Rescission can wipe out the finance charge and in some cases the loan balance itself.

- Statutory damages. TILA allows homeowners to recover money from lenders who violate disclosure rules.

- Loan balance reduction. In some cases, legal review of a flawed loan can reduce what you owe, particularly when the dealer fee was not properly included in the APR.

- Debt relief. Through negotiated legal resolution, some homeowners have had their solar loan balances forgiven entirely. This is not guaranteed and depends heavily on your specific loan, your state, and how your loan was sold.

- Attorney's fees. TILA allows prevailing homeowners to recover legal costs from the lender, which is why qualified legal teams will take these cases seriously.

You should be careful with anyone who promises loan forgiveness up front. No honest advocate can look at your situation and guarantee that outcome. What a senior consultant can do is review your loan documents, look for TILA issues, and tell you what relief you may qualify for. From there, legal review determines the path forward.

What To Do Next

- Find your solar loan paperwork. You want the Truth in Lending disclosure, the loan agreement, and the installation contract. If you do not have copies, request them from your lender in writing.

- Write down three numbers: the cash price of the system, the total financed amount, and your monthly payment times the number of months.

- Compare the interest rate to the APR. Note the gap.

- Search the documents for the words "dealer fee," "origination fee," or "platform fee." Note whether they appear, and if so, for how much.

- Get free Solar Relief Assessment. A senior consultant can review your loan, identify possible TILA violations, and walk you through what relief you and your family may qualify for.

Common Questions About Hidden Dealer Fees

Are dealer fees in solar loans illegal?

Dealer fees themselves are not illegal. What may be illegal is hiding them, failing to include them in the APR, or misrepresenting the true cost of the loan. That is a potential TILA violation.

My contract never said "dealer fee." Does that mean there isn't one?

Not necessarily. Dealer fees are often rolled into the system price rather than listed as a separate line item. That is part of the problem. A review of your paperwork, cash price, and payment math usually reveals whether a dealer fee is present.

What is the difference between a solar loan and a solar lease?

A solar loan means you are financing the panels and you own them at the end. A solar lease means you are renting the panels from a company that owns them. Loans usually have a fixed monthly payment. Leases often have an annual escalator that raises your payment every year. Both can have their own disclosure issues.

Can my solar loan really be forgiven?

In some cases, yes. When a loan contains serious TILA violations, legal resolution can lead to loan balance reduction or full forgiveness. This is not a guaranteed outcome. Every loan is different. A qualified consultant and legal review can tell you what is realistic in your specific situation.

Can I just stop paying my solar loan?

No. Stopping payment can damage your credit, trigger collection actions, and put your home at risk if the loan is secured. Always talk to a qualified consultant before changing anything about your payment situation.

How long do I have to act?

TILA has specific time limits. The right to rescind a home-secured loan for undisclosed charges can extend up to three years from the date you signed. Statutory damages usually have a one-year window. If you think your loan has a problem, do not wait to have it reviewed.

Is Solar Home Advocate a law firm?

No. Solar Home Advocate is a consumer education and advocacy resource. We connect homeowners with legal review when a situation calls for it. We do not provide legal advice ourselves.

Sources & References

Truth in Lending Act, 15 U.S.C. § 1601 et seq. Consumer Financial Protection Bureau, guidance on solar financing and dealer fees (2023). Federal Trade Commission, residential solar consumer protection guidance. New Mexico Attorney General consumer protection filings. Connecticut Department of Banking enforcement actions. Minnesota Attorney General deceptive practices actions. Federal court class action filings against major solar lenders. Solar Energy Industries Association industry data.

Still Paying a Solar Loan AND a High Electric Bill?

If the savings your salesperson promised never showed up - or if you're not sure what's actually in your loan - the first step is having someone review your situation. A senior consultant will walk you through what relief you may qualify for.

Free Assessment

Find out what options are available to you. A senior consultant will review your situation and walk you through your next steps.

Hidden dealer fees are in almost every solar loan. If yours weren't properly disclosed, that could be a Truth in Lending Act violation - and that changes your options.