The 'Escalator Clause' in Your Solar Contract - and How Much It's Quietly Costing You

There is a single line in most solar contracts that raises your monthly payment every year - and there's a good chance your solar salesperson didn't take the time to explain this to you.

It's called the escalator clause.

This single line raises your payment every year by roughly 2.9%. Some contracts go as high as 4.9%. That might not sound like much. But over time, have a look at how this adds up for you and your family.

What an Escalator Clause Is, in Plain English

An escalator clause is a section of your solar lease, PPA, or loan that says your monthly payment will go up by a fixed percentage every year for the life of the contract. Most solar contracts run 20 to 25 years.

Here is what those terms mean:

- Lease: You rent the panels from a solar company. They own them. You pay a monthly fee.

- PPA (Power Purchase Agreement): You buy the electricity the panels produce, not the panels themselves. You pay per kilowatt-hour.

- Solar loan: You finance the panels. You own them at the end. You pay a monthly loan payment.

Escalator clauses show up most often in leases and PPAs. But they can also appear in loans as variable rate adjustments. The key thing to look for: any language that says your payment goes up year after year, automatically.

What 2.9% Actually Looks Like Over 25 Years

Let's say you're paying $150 a month right now. With a 2.9% annual escalator clause on a 25-year lease, here's what happens:

- Year 1: $150/month

- Year 5: $168/month

- Year 10: $194/month

- Year 15: $224/month

- Year 20: $259/month

- Year 25: $299/month

That's your $150 payment turning into nearly $300. Over the full 25 years, you pay about $63,000 in solar payments alone.

And that's just at 2.9%. At 4.9% (which is in many contracts), that same $150 payment becomes more than $480 by Year 25, and your total solar payments climb to nearly $90,000.

Most homeowners don't even notice this until they compare their current bill to what they actually signed up for. By then, they've usually been paying for years.

Why Solar Companies Put Escalators in Your Contract

Solar companies include escalator clauses to keep pace with projected electricity rate increases. The pitch is simple: even with your rising solar payments, you're still "saving" compared to what you'd pay the utility company.

The problem is that electricity rates don't always go up at 2.9% per year.

Over the last decade, the national average residential electricity rate has increased roughly 2% per year, according to the U.S. Energy Information Administration. In many states, the increase has been slower. Arizona has averaged about 1.8% per year. Nevada about 1.7%. That means your solar payment can climb faster than what the utility company is actually charging. And the gap gets wider every year.

So the thing your solar deal was supposed to save you money on stops saving you anything at all. Eventually, you start losing money on the deal.

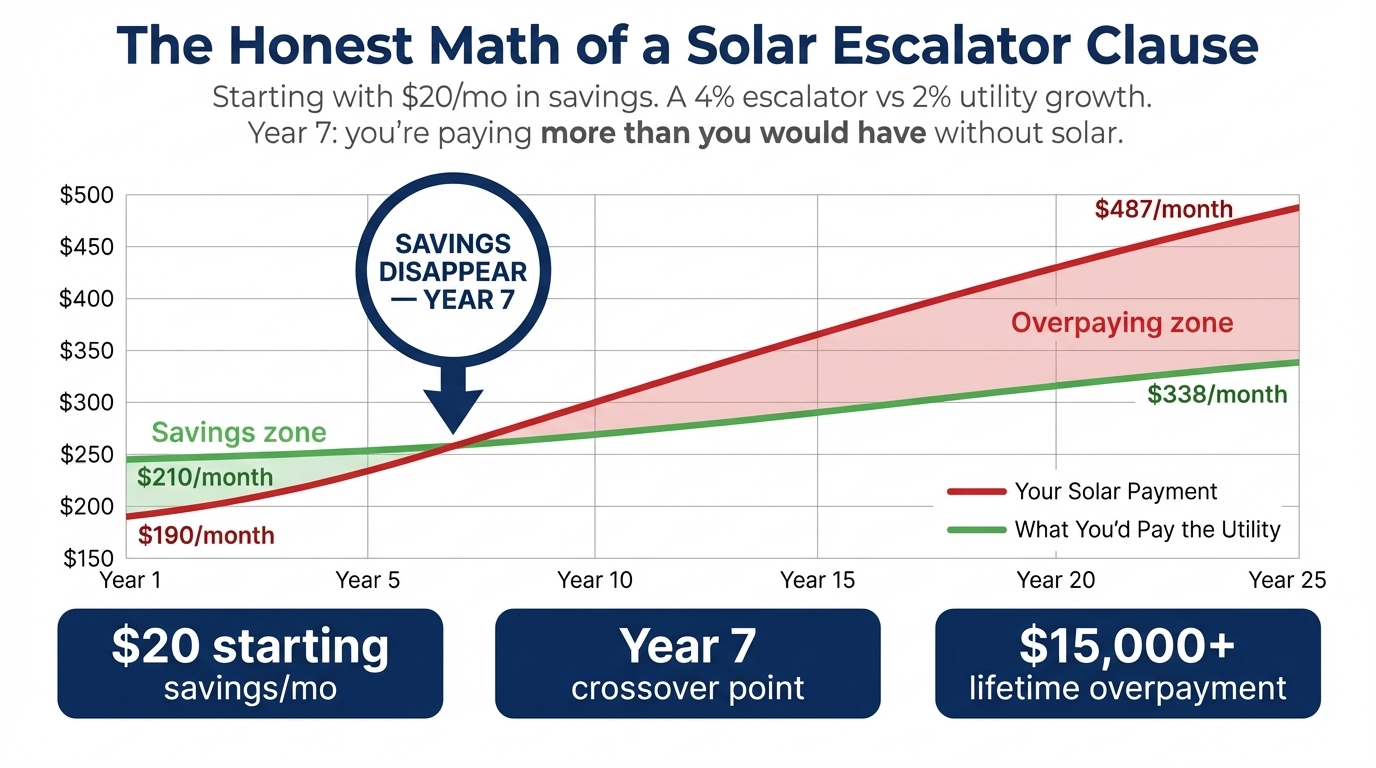

Where Your "Savings" Disappear

Here's what nobody tells you when you sign:

If your solar payment escalates at 4% per year and your local utility rate rises at 2% per year, you can hit a break-even point as early as Year 6 or 7 of your contract. From that point on, you're paying more for solar than you would have paid the utility company.

That's not a glitch. That's how the math works on most contracts. The salesperson just didn't run those numbers in front of you.

Over a 25-year contract, the total amount you overpay (compared to what you would have paid the utility) can be $15,000 or more. For families on fixed incomes, that's not a small problem. That's a retirement-level number.

Real Examples From the Industry

Escalator clauses have been at the center of major regulatory actions and lawsuits across the country.

- The New York Attorney General's office has investigated multiple solar companies for misleading consumers about long-term costs, including escalator clause disclosures.

- The California Public Utilities Commission has received thousands of complaints from homeowners citing payments rising faster than they were told.

- The Federal Trade Commission has flagged escalator-clause marketing as a top concern in residential solar.

- State attorneys general in Texas, Florida, and Illinois have all filed actions against solar companies for failure to clearly disclose escalating costs.

You are not the only homeowner who didn't have this clearly explained to you. You are part of a much larger pattern.

How to Find an Escalator Clause in Your Own Contract

Pull out your solar contract and look for language like this:

- "Annual price escalator"

- "Annual rate adjustment"

- "Escalation factor"

- "Annual increase percentage"

- "Annual lease payment adjustment"

- "Year-over-year rate increase"

It's usually in the section labeled Payment Terms, Lease Payments, or Pricing Schedule. Sometimes it's in a payment chart at the back. Sometimes it's in fine print on a single line.

If your contract says your monthly payment increases by any percentage annually, you have an escalator clause. If you can't find it - or can't make sense of the legal language - that's exactly what a Free Assessment is for.

What You Can Actually Do About It

If you have an escalator clause and you weren't clearly told about it before signing, you may have options. What you can do depends on three things:

- Your state. Some states (like California, New York, and Texas) have stronger consumer protection laws around solar contracts than others.

- Your contract type. Lease, PPA, and loan disputes follow different rules.

- How the clause was presented to you. If the salesperson promised your payment would never go up, told you the escalator would be "small," or skipped over it entirely, that may be grounds for a contract dispute under deceptive trade practice laws.

Possible paths forward include:

- Renegotiating the contract terms with the solar company

- Filing a complaint with your state attorney general's consumer protection division

- Filing a complaint with the Better Business Bureau

- Joining an existing class action lawsuit if one is open in your state

- Pursuing an individual claim under your state's deceptive trade practices act

None of these are quick. Most take months. But homeowners around the country are getting contracts modified, payments reduced, and in some cases, contracts cancelled outright.

What To Do Next

- Find your solar contract. If you don't have a copy, request one from your solar company in writing.

- Look for the words above. Highlight any language about annual increases.

- Calculate what your payment will be in Year 10, Year 15, and Year 25 using the escalation rate in your contract.

- Compare that to your current monthly utility bill (before solar) plus 2% per year.

- If the gap is significant - or if you can't tell what your contract actually says - get a Free Assessment. A senior consultant can review your contract and walk you through what you're actually looking at.

Common Questions About Escalator Clauses

Is an escalator clause illegal?

No. Escalator clauses themselves are legal in most states. What may be illegal is failing to clearly disclose the clause, or making misleading claims about long-term costs during the sales process.

I was told my payment would stay the same. What can I do?

If a solar salesperson told you your payment would never go up, or told you the escalator was "small" or "no big deal," that may be grounds for a contract dispute under deceptive trade practice laws in your state. Document what you were told if you can.

Can I just stop paying?

No. Stopping payment can damage your credit, trigger collection actions, and complicate any dispute. Talk to a qualified consultant before changing anything about your payment situation.

Does an escalator clause apply if I bought my panels with a loan?

Most solar loans have a fixed monthly payment, not an escalator. But some have variable rates that can adjust over time. Check your loan agreement for any annual rate adjustment language.

What if I want to sell my house?

An escalator clause makes a solar lease or PPA harder to transfer to a new buyer. Many buyers refuse to take over a contract with rising payments. Some lenders refuse to fund a mortgage on a home with an attached solar lease. We cover this in detail in our Home Sale Trap article.

Will the solar company just cancel my contract if I ask?

Almost never. Most solar companies will not cancel a contract just because you ask. That's why understanding your legal options matters.

Sources & References

U.S. Energy Information Administration, Electric Power Monthly. New York Attorney General's office, consumer protection actions. California Public Utilities Commission, complaint database. Federal Trade Commission, residential solar guidance. Texas, Florida, and Illinois Attorney General consumer protection filings. Solar Energy Industries Association, industry data.

Want To Know If Your Contract Has an Escalator Clause?

If any of this sounds familiar - or if you're not sure what's in your contract - the first step is talking to a senior consultant who can review your situation and tell you what relief you may qualify for.

Free Assessment

Talk to a senior consultant who can review your contract and tell you what relief you may qualify for.

No cost. No obligation. No pressure.

Sal Says

"A 2.9% escalator clause on a 25-year lease can nearly double your monthly payment. Most homeowners don't find out until it's too late."