"Free Solar" Isn't Free. Here's What You Actually Signed.

If someone came to your door and told you they could put solar panels on your roof for free, they weren't exactly lying. But they weren't telling you the whole truth either.

"Free" doesn't mean you own the panels. It means someone else owns them, puts them on your roof, and you pay that company every month for the next 20 to 25 years.

That's not free. That's a long-term financial contract tied to your home. And for hundreds of thousands of families across the country, it's the single largest purchase they've made after their house and their car.

What "Free Solar" Actually Means, in Plain English

"Free solar" is a marketing phrase. It is not a legal product. When a sales rep uses the word "free," they almost always mean one of three things:

- You pay $0 out of pocket the day the panels get installed.

- You sign up for a monthly payment that is supposed to be lower than your current electric bill.

- You qualify for tax credits or rebates that someone else, not you, is going to collect.

None of those three things are the same as "free." In every case, there is a 20 to 25 year financial obligation attached to your roof. The only question is who owns the panels, who collects the tax credits, and how the payment is structured.

The Federal Trade Commission has flagged "free solar" language as a common source of consumer complaints. The Better Business Bureau lists residential solar as one of the most-complained-about industries in the country, with thousands of new complaints filed every year.

Why Companies Use the Word "Free" and Who Gets Caught By It

The residential solar industry exploded between 2016 and 2023. According to the U.S. Energy Information Administration, small-scale solar capacity more than tripled during that stretch. Most of that growth came from door-to-door sales and high-pressure phone campaigns aimed at homeowners over the age of 50.

Sales reps are paid on commission. On a typical residential solar deal, the dealer fee and commission together can run $10,000 to $20,000, baked directly into the price you end up paying. The faster a rep closes you, the faster they get paid. That is why the pitch is usually short, fast, and built around one word: free.

The people who get hit hardest are retirees, homeowners on fixed incomes, and families in states with rising electricity rates like Arizona, Nevada, Texas, and Florida. The pitch lands because the promise sounds simple. The reality underneath the pitch is anything but.

The Three "Free Solar" Structures

Almost every "free solar" pitch ends in one of three contracts. Each one works differently. Each one has a different definition of what is actually free.

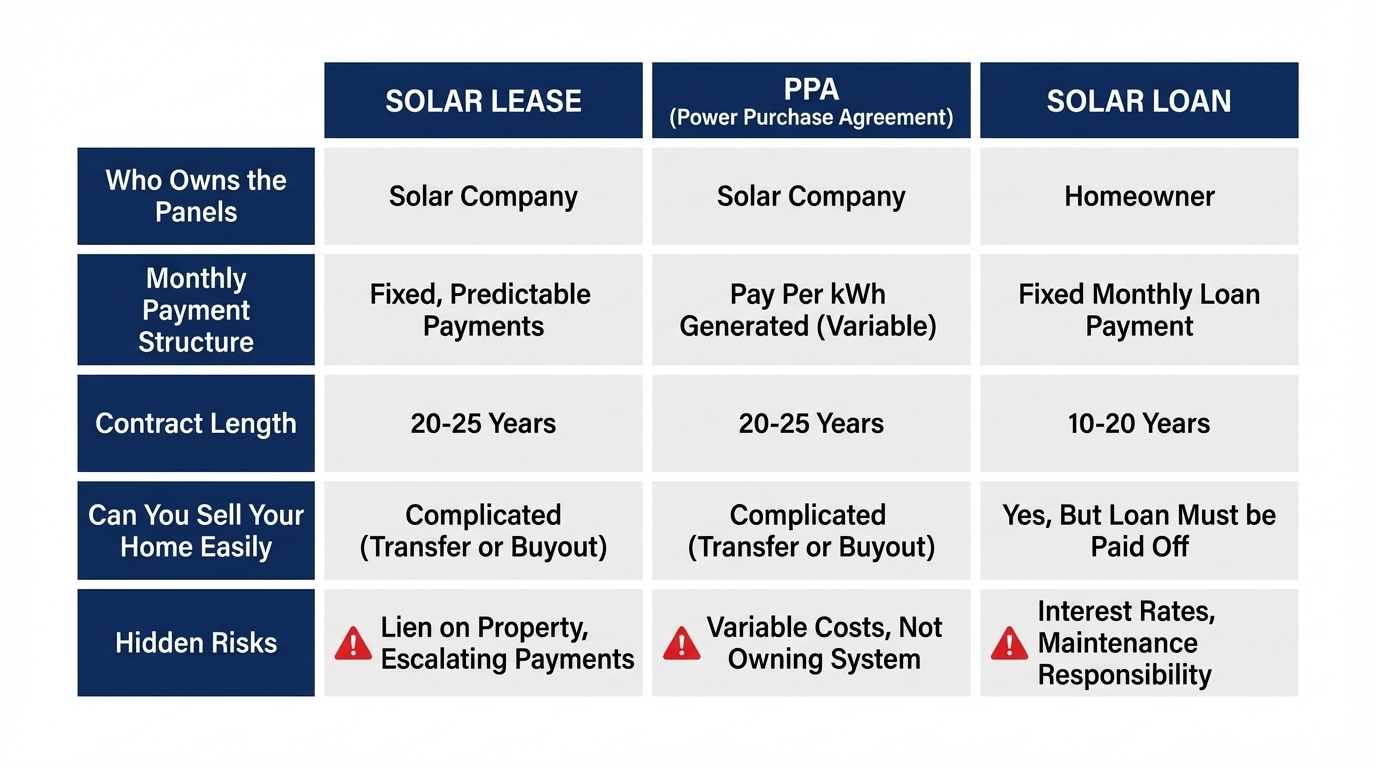

1. The Solar Lease

With a lease, the solar company owns the panels. You rent them. You pay a flat monthly fee, usually for 20 or 25 years.

What's "free": The equipment, the installation, and the roof work on day one. You do not write a check at signing.

What you pay: A monthly lease payment, often starting around $90 to $200. That payment usually goes up every year under an escalator clause, typically 2.9% annually.

What you do not get: The federal solar tax credit. The state rebates. Any Solar Renewable Energy Credits (SRECs). All of those go to the company that owns the panels, not to you and your family.

2. The Power Purchase Agreement (PPA)

A PPA is close cousin to a lease. The solar company owns the panels. Instead of a flat rent, you pay for the electricity the panels produce, measured in kilowatt-hours.

What's "free": The hardware, the install, and the upfront cost.

What you pay: A per-kilowatt-hour rate for everything the system generates. That rate usually escalates 2% to 4% per year. If the system produces more than your home uses, you still pay for what it produced.

What you do not get: The tax credits, the rebates, and the ability to unplug the system without penalty.

3. The Solar Loan

With a loan, you own the panels at the end. But you are financing them, and the total is bigger than most homeowners realize. A typical residential solar loan runs $30,000 to $50,000 over 20 to 25 years.

What's "free": Nothing. The word "free" in a loan pitch usually refers to $0 down at closing.

What you pay: A fixed monthly loan payment, plus your regular electric bill in most months, plus any "dealer fee" that got rolled into the loan balance. Dealer fees of $5,000 to $15,000 are common and are often not broken out clearly on the paperwork you sign. The Truth in Lending Act (TILA) requires clear disclosure of finance charges. If your fees were not disclosed properly, that is a federal issue.

What you keep: The federal Residential Clean Energy Credit (30% of the system cost) and any state rebates, if you have the tax liability to use them.

Real Cases, Real Companies, Real Consequences

This is not theoretical. Regulators and courts have been working through "free solar" complaints for years.

- Pink Energy (formerly Power Home Solar) shut down in 2022 after state attorneys general in North Carolina, Missouri, Kentucky, and Virginia took action over deceptive sales practices. Thousands of customers were left with loans on equipment that never worked right.

- Titan Solar Power, once one of the largest installers in the country, filed bankruptcy in 2024, stranding tens of thousands of customers mid-project.

- ADT Solar (formerly Sunpro) was shut down by its parent company in 2024 after years of consumer complaints over sales practices and system performance.

- SunPower, a household brand, filed Chapter 11 bankruptcy in 2024. Customers with leases and PPAs were forced to navigate the bankruptcy process to figure out who now owned the contract on their roof.

- Infinity Energy has been the subject of multiple state attorney general investigations over high-pressure sales and misrepresented savings.

- The New York Attorney General's office has reached settlements with multiple solar companies over misleading "free solar" and savings claims.

- The California Public Utilities Commission has received thousands of complaints about residential solar sales practices since 2020.

According to industry reporting, more than 100 residential solar companies have filed bankruptcy or shut down since 2023. The contracts those companies wrote did not disappear with them. They got sold to loan servicers, lease portfolios, and investor groups. The homeowner still owes the money. That is the part the pitch left out.

How to Spot "Free Solar" Language in Your Contract

Pull out your contract. Look at page one and the first few pages that follow. Here is what tells you what you actually signed:

- "Solar Lease Agreement" at the top of page one means the solar company owns your panels.

- "Power Purchase Agreement" or "PPA" means the solar company owns your panels and you buy the power.

- "Retail Installment Contract," "Loan Agreement," or "Promissory Note" means you own the panels and you owe a lender.

Then look for these phrases. Any of them tells you the deal is more complicated than "free":

- "Dealer fee" or "origination fee"

- "Annual escalator" or "annual rate adjustment"

- "System price" that is $10,000 or more above the equipment cost

- "Production guarantee" with fine print about what happens if the system underperforms

- "Assignment" clauses that let the company sell your contract to another party

- "Buyout" or "early termination" fees

If the word "free" appears anywhere in your marketing materials but your contract has any of the language above, those two documents are not telling you the same story.

What You Can Actually Do About It

If you were told the deal was free and the paperwork tells a different story, you have options. What is available depends on your state, your contract type, and how the sale was presented to you.

Here is the landscape:

- Home Solicitation Act protections. Most states give you a 3-day right to cancel any contract signed at your home. Some states extend that to 5 or 7 days for seniors. If you are still inside that window, you may be able to cancel outright.

- State deceptive trade practices acts. Every state has one. If a salesperson told you the panels were free, promised savings that never showed up, or skipped over the escalator clause, that may qualify as a deceptive trade practice.

- Truth in Lending Act (TILA) violations. On a solar loan, if dealer fees were not disclosed correctly or the finance charge was understated, TILA gives you federal remedies, including potentially rescinding the loan.

- State attorney general complaints. Every state AG has a consumer protection division. They pay attention to solar. Filing a complaint puts your case on the record.

- Better Business Bureau complaints. Not a legal remedy, but it creates pressure and a paper trail.

- Class action participation. Lawsuits are active in California, Texas, Florida, New York, and other states. You may already qualify.

States with stronger solar-specific consumer protections include California, New York, Connecticut, New Jersey, and Massachusetts. States with weaker protections, like Florida, Texas, and Arizona, lean more heavily on general deceptive trade practices law. Every state has something. You just have to know where to look.

What To Do Next

- Find your contract. If you do not have a copy, request one in writing from the company that installed your system. Federal and state law require them to give it to you.

- Identify what you signed. Lease, PPA, or loan. Write it down on the first page.

- Add up the 25-year total. Take your monthly payment, multiply by 12, multiply by 25. If there is an escalator clause, the real total is higher. That is what "free" actually cost.

- Compare to the salesperson's promise. Did they tell you a total cost? Did they tell you your utility bill would go to $0? Did they call the panels "free"? Write down what you remember. If you have text messages, voicemails, or emails, save them.

- Get free Solar Relief Assessment. A senior consultant can review your contract, tell you what structure you actually signed, and walk you through whether you qualify for relief. No cost. No obligation.

Common Questions About "Free Solar"

If my salesperson said solar was free, did they break the law?

Not automatically. The word "free" by itself is a marketing term. What can cross the line is the full picture: promising savings that were not realistic, skipping over the escalator clause, hiding dealer fees, or telling you your electric bill would go to zero. Those claims, taken together, can support a deceptive trade practices case in most states.

I have a lease and I want out. Can I just remove the panels?

No. The panels belong to the solar company. Removing them without approval can trigger penalties and legal action. The right move is to review your contract, document what you were told, and get an assessment before making any changes.

I have a solar loan. Do I really own my panels?

Yes, in the legal sense. You hold title to the equipment. But the lender holds a financial interest until the loan is paid off. If the loan has undisclosed dealer fees or TILA violations, the loan itself can sometimes be challenged even though the panels are yours.

What are "dealer fees" and why are they a problem?

A dealer fee is a charge the solar company pays the lender to offer you a low advertised interest rate. That fee, sometimes 20% to 30% of the system price, gets added to your loan balance. Many homeowners were never told the fee existed. Under the Truth in Lending Act, finance charges and the real cost of credit have to be clearly disclosed. If they were not, that is a federal issue.

The company that installed my panels went bankrupt. Do I still owe the money?

In most cases, yes. Your lease, PPA, or loan was almost certainly sold to another company. That company now collects the payments. The workmanship warranty, though, often disappears with the original installer, which leaves you paying for equipment nobody is responsible for fixing.

Can I get my tax credit back if a company took it?

If you signed a lease or PPA, the company owns the system and the tax credit legally belongs to them. You cannot get it back. What you can do is review whether the sales pitch implied the credit was yours. If it did, that becomes part of a deceptive practices claim.

Is it worth fighting this if my monthly payment is manageable?

That is a personal call. But understand what is at stake: a 25-year contract at $150 a month with a 2.9% escalator totals about $63,000. At $200 a month with a 3.9% escalator, the 25-year total is over $95,000. "Manageable" today is not the same number as "manageable" in Year 20.

Sources & References

U.S. Energy Information Administration, small-scale solar capacity data and Electric Power Monthly. Federal Trade Commission, residential solar consumer guidance. Better Business Bureau, residential solar complaint data. New York Attorney General's office, consumer protection settlements. California Public Utilities Commission, complaint database. Truth in Lending Act (15 U.S.C. 1601). State Home Solicitation Acts and state deceptive trade practices statutes. Court filings and press coverage on Pink Energy, Titan Solar Power, ADT Solar, SunPower, and Infinity Energy. Internal Revenue Service guidance on the Residential Clean Energy Credit.

Not Sure What Kind of Solar Deal You Signed?

Most homeowners don't know if they signed a lease, a PPA, or a loan - and their salesperson didn't explain the difference. If you want someone to walk you through what you actually signed and what it means for you and your family, start here.

Free Assessment

Talk to a senior consultant who can review your contract and tell you what relief you may qualify for.

No cost. No obligation. No pressure.

Sal Says

"If someone told you solar was 'free,' you probably signed a lease or PPA. That means a company owns the panels on your roof - and you're paying them every month for the next 20 to 25 years."